Economic growth

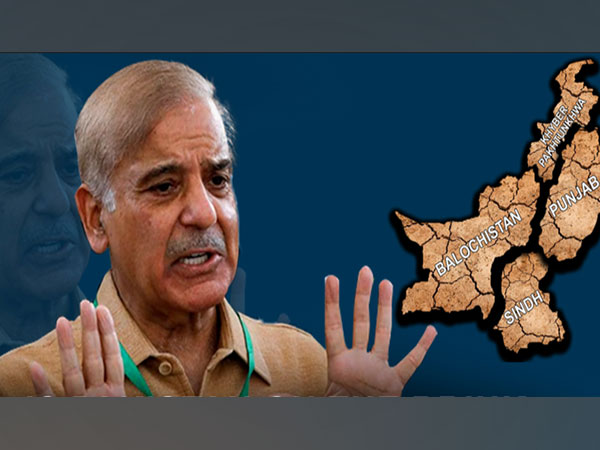

Can Pak’s Economic Crisis Lead To Its Balkanisation?

‘I Know Little About Economy, But I Am Managing Fine’

A day in the life of Naveen, a mobile accessories seller in Delhi

We Will Be Lucky To Get 5% Growth Next Year: Rahugram Rajan

India-UK Free Trade Agreement On Cards

Taliban Sign Deal For Russian Oil, Gas, And Wheat At Discounted Rate

Get the latest stories in your inbox

FDI Inflows To Cross $100 BN In 2022-23

Weekly Update: Healthcare & Growth Are Two Things Modi Must Focus On

Economic growth

No description available.

7 Articles